WARC‘s latest research paper, Global Ad Trends: Media’s New Normal, reveals that there is perhaps less reason to be gloomy than the wider economy suggests. Despite recent struggles in the wider advertising sector and economies as a whole, the marketing effectiveness research body has found that global advertising spend is now on course to close out 2025 with growth of 8.9% to $1.19trn, an upgrade of 1.5 percentage points (pp) from WARC’s September forecast due to strong results from Big Tech platforms and a muted impact on global trade from trade tariffs.

A further rise of 9.1% (+1.0pp since September) to $1.30trn is forecast next year, while growth of 7.9% (+0.8pp) in 2027 would push the market’s value to $1.40trn – a doubling in size since the pandemic and equivalent to $150 spent for every person alive today.

Alex Brownsell, Head of Content, WARC Media and author of the report, says: “Advertising has broken away from the economic cycle, and behaves in a way that doesn’t feel reflective of the real economy. New money has arrived from digital-native categories, while commerce has redrawn the measured media map, and Big Tech’s self-reinforcing flywheel is harvesting almost all incremental dollars.”

The latest forecasts show that the benefits of strong global growth prospects will not be evenly distributed. Alphabet, Meta and Amazon will collectively absorb the vast majority of incremental global ad spend between 2025 and 2027, increasing their share of the global ad market excluding China to 58.8% by the end of the forecast period.

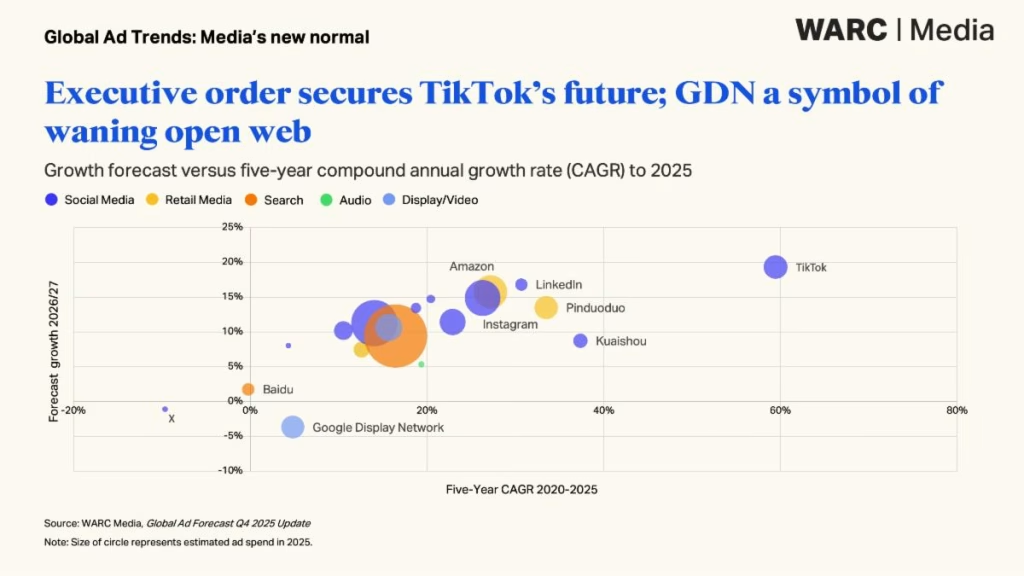

A handful of emerging online platforms, such as TikTok and Reddit, are an exception, growing faster than the incumbents to gain share but from a far lower base. TikTok is on course to net $45.2bn in ad revenue by 2027, but this is less than a fifth of Meta’s expected ad revenue at that time. An executive order signed in September 2025 stands to remove the uncertainty around TikTok’s future in the US, by far its largest trading market at approximately $12bn this year.

The favouring of Big Tech is partly down to fee layers in advertising shrinking, so more of each ad dollar now goes straight to the large platforms, as noted by Brian Weiser, Principal, Madison & Wall. This boosts Big Tech revenue even when total spending is flat. Lower creative costs (due to the wider availability of AI tools), tighter agency margins, and cheaper ad-tech services are also contributing to the ongoing prosperity of Big Tech platforms in the coming years.

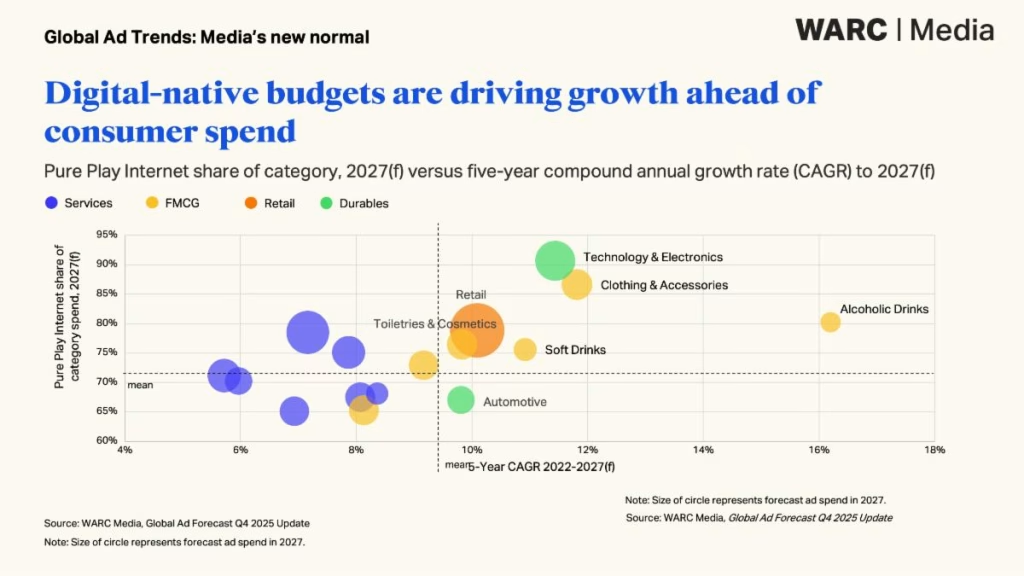

A new wave of digital-native budgets has flowed into platforms, creating a second engine of growth that had little connection to household spending power. Small and medium-sized businesses, trade-marketing funds and retail media networks have brought billions into digital ecosystems that promise accountability and speed.

Clothing & Accessories provides a clear example: more than 80% of spend in the sector now flows straight into retail media, paid search, and social platforms. In other words, almost all the incremental growth is being captured by platforms, not traditional channels. Technology & Electronics is another fast-growing vertical whose investment is highly measurable and is structurally predisposed to spend at the bottom of the funnel.

For the wider market, this creates a two-speed system: legacy categories whose spend is broadly stable, and new categories whose explosive growth flows disproportionately to the major platforms, further accelerating the structural shift of ad dollars into digital ecosystems.