By Tom Stoten, Director at finnCap Cavendish

Over the past few months, there has been a decline in deals due to uncertainty in the political and macroeconomic landscape. However, we are now witnessing a positive shift in sentiment and an increase in conversations, particularly among founder-backed businesses in the UK. These businesses are concerned about the potential outlook for Capital Gains Tax following an anticipated General Election in Q4 2024. In the past, we have learned that the market has limited capacity to consider new transactions, as seen in the period from September 2020 to March 2021 when many deals failed to materialize due to the volume in the market at that time.

More positively, there is a continued trend of moving away from sectors heavily dependent on consumer discretionary spending and towards more resilient sectors like technology. When this is combined with a significant amount of capital within Private Equity funds, in particular, due to the deployment of capital being slower than expected, transactions that possess specific desirable characteristics listed below are still able to command premium valuations:

- Strong organic growth prospects

- Demonstrable profitability and cash generation

- A unique market position, often with a strong focus on specific verticals

- High levels of recurring revenue and strong customer relationships

- Successful land and expand strategies within their client base.

Differences between sub-sectors within technology

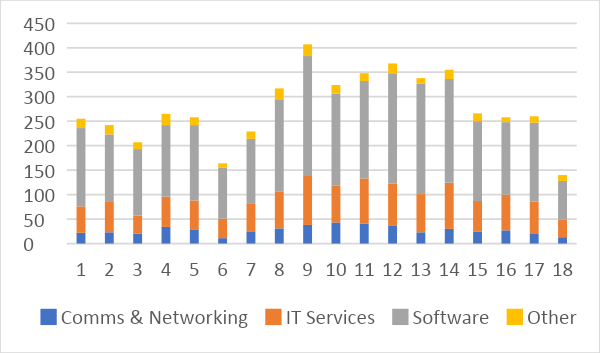

The highest M&A transaction volume in the UK was observed in Q1 2021, which interestingly aligns with the period when interest in the sector was particularly high due to the wider digitalisation ongoing in the economy.

However, when looking at M&A within the broader technology sector, we must consider many different dynamics. A quick look at three sub-sectors – IT Managed Services, Digital Transformation consultancies and Software – can help depict diverging performance and drivers of M&A.

IT Managed Services

IT Managed Services as a sub-sector continues to display remarkable resilience and steady growth rates, hovering around the mid-teens. Businesses now seek reliable outsourced IT partners who can offer a comprehensive range of solutions to keep up with increasing digitisation and the rapidly evolving market. At the C-Suite level, there is a notable shift in perception, viewing it not merely as a cost but as a fundamental element supporting technology delivery to enhance value creation, customer and user experiences, which in focus will fuel further growth opportunities.

Providers that can showcase areas of differentiation, whether horizontally through specific platform capabilities or vertically through specialized sector knowledge and delivery expertise, will remain in high demand and enjoy continuous growth. Consequently, valuation multiples have remained robust over the past two years, particularly for assets that check all the right boxes. However, managed service providers solely focused on building scale without demonstrating strong organic growth are an exception to this trend. As the cost of capital increases, showcasing strong organic growth has become imperative for providers adopting a buy-and-build strategy.

Digital Transformation Consultancies

In 2023, Digital Transformation consultancies faced challenging trading conditions due to their business model’s nature, with the need to build capacity and bench depth in anticipation of contract wins compounded with demand side pressures causing a hesitance to commit to some large programs. As a result, a number of listed companies (such as Endava) downgraded their forecasts multiple times Despite the overall challenges, certain areas in the industry experienced strong growth. Notably, companies specializing in the application layer and high growth vendor ecosystems will benefit from the tailwinds.

Software

Within software, there is a clear trend towards quality with investors emphasizing metrics such as ARR (Annual Recurring Revenue), gross and net revenue retention, and above all, profitability rather than excessive cash burn in pursuit of growth. Valuations for both horizontal (targeting specific business areas like HR) and vertical (focused on particular end markets) software remain robust, as investors seek opportunities that can disrupt markets without constant cash infusions. Whilst, the number of deals in the UK software sector has declined below the 5-year average in the last three quarters, reflecting a recalibration among investors towards sustainable and disruptive opportunities rather than rapid, cash-intensive growth, we still see significant interest in businesses that display these characteristics.

The next 12-24 months

We remain optimistic about the outlook for the next 18 months given our recent conversations in the market. There remains significant amounts of interest in the technology sector however the need to prepare thoroughly before launching a process to achieve both a premium valuation and a successful transaction remains, particularly in an environment where the market is expected to be busier into 2024.

Looking especially among the different sub-sectors, managed services have seen plenty of activity. With more providers becoming one-stop shops for the customer to retain both share of customer wallet and of customer mind, we expect this strong activity to continue. From a value perspective, project services has too often been viewed as inferior to recurring revenue. Yet, as cloud implementation drives a need for customers to revisit their IT systems, providers are and will continue to, capture customer mind share and prioritise they do not get separated by other partners coming in.

We expect further consolidation within the digital transformation sub-sector as large service integrators will acquire specialist capabilities for cross-selling opportunities as well as scale to deliver pipelines. Consultancies, which have seen pipeline challenges of late, will seek growth through scale, new capabilities and geography and therefore we expect digital transformation to be a relatively hot area by acquisition volume.

Software valuations are unlikely to return to those seen in 2020/21. Despite this, there will continue to be a large support for quality supporting valuations at the top end of the market. We believe transaction volumes in this sub-sector are likely to remain robust, due to both a continued desire to invest capital into this sub-sector as well as founders aiming to take capital off the table ahead of potential tax changes.